H. 3579 Overview

The House Ways and Means full committee today voted to combine the two bills related to roads and income tax. The bill now moves to the whole House under H. 3579. Through the floor debate and amendment process it may experience changes. The below facts, figures, and estimates provided by the House Ways & Means Committee reflect H. 3579’s current makeup.

1. Restructuring: There are two key components to restructuring in H. 3579. The first restructures the Department of Transportation and the second component restructures the State Infrastructure Bank.

A. Department of Transportation (DOT)

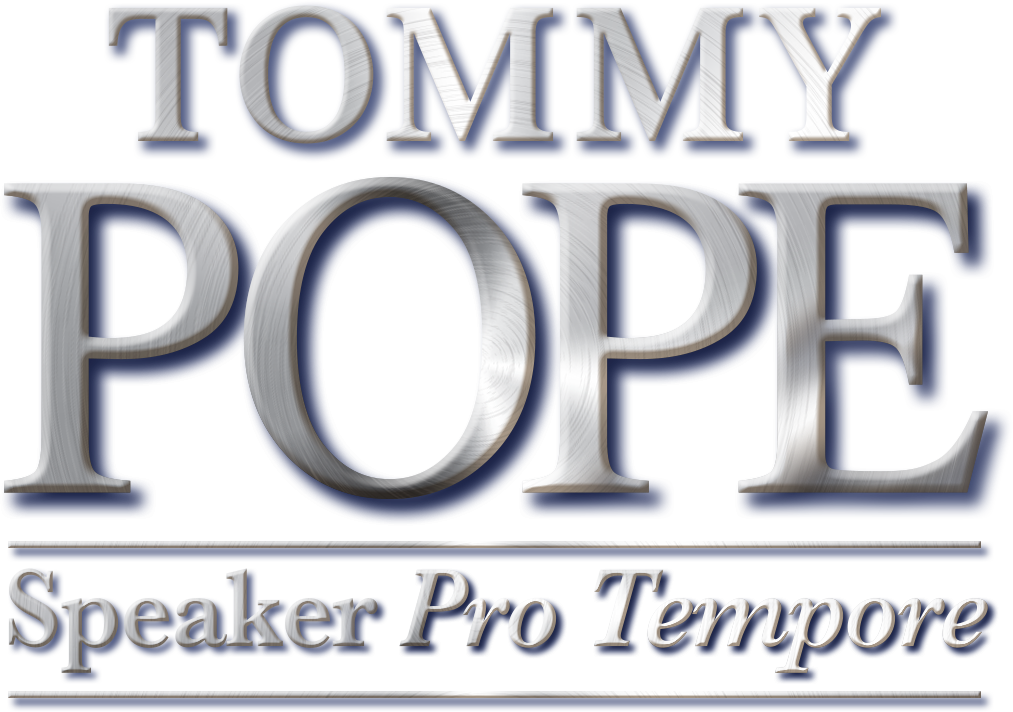

- The Governor appoints Highway Commissioners (7 districts and 1 statewide) with a Joint Transportation Review Committee screening process approval. These commissioners serve at the pleasure of the Governor. The Highway Commission will then appoint a secretary with the advice and consent of the Senate. Commissioners hold no “terms” and may only serve a combined 12 years on the commission (retroactive).

B. State Transportation Infrastructure Bank (SIB)

- The SIB Board expands from 7 to 13 members. It would consist of 7 district highway commissioners, 3 appointments from the Speaker of the House, and 3 appointments from the Senate President Pro Tempore. Of those appointments from legislative bodies, 1 of each must be an ex officio Representative and Senator. SIB members would have no terms and may only serve a combined 12 years (retroactive).

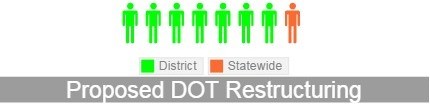

- The SIB would lower its current $100 million project minimum to a $25 million project minimum and must follow project prioritization set forth by the South Carolina Department of Transportation in accordance with ACT 114. Only a Joint Resolution can override prioritization criteria requirements. However, only one project may be re-prioritized in a single Joint Resolution.

2. Transfer of Local Roads: Local governments that wish to take ownership of local roads (as identified by SCDOT) in their political subdivision may do so. In doing so, these local governments would be eligible for additional C-Funds. Should local governments opt in to take ownership of additional roads, they would receive transferred roads in three phases:

- Phase 1: Local governments select 1/3 of identified roads in 2016.

- Phase 2: Local governments select 1/3 of identified roads in 2018.

- Phase 3: Local government select final 1/3 of identified roads in 2020.

- As part of the phase-in process, the monies allocated to participating local governments would see an increased C-fund allocation of $1 million in year one followed by additional revenue increases in phase 2 and phase 3. Participants who opt in during phase 2 in 2018 would see a $500,000 annual increase in C-funds. Finally, participants who opt-in during the final phase would see a $250,000 annual increase in C-funds. C-funds would no longer come with a mandate requiring a percentage of funds be spent on state roads; this decision would rest with local decision makers.

3. Funding Components: There are two funding components.

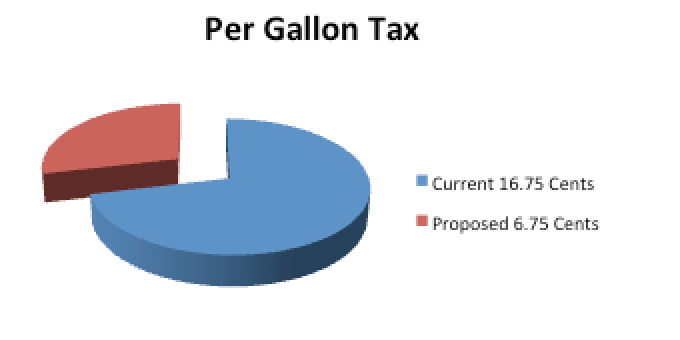

A. Gas Tax

1. Per Gallon Tax – Currently it is 16.75 cents per gallon of motor fuel (gasoline and

diesel). This proposal would drop it to 10.75 cents per gallon of motor fuel.

2. Excise Tax – A wholesale indexed excise tax of 6% would be applied to a 6-month

average of the wholesale price of motor fuel.

B. Auto Sales Tax – Currently the auto sales tax is 5% of total vehicle costs capped at $300. This proposal would raise that cap to $500. Currently the auto sales tax is broken down with 20% going to education, 40% to the DOT, and 40% to the General fund. Under this proposal, the 20% capped at $300 for education remains, the 40% of the $300 designated to the General Fund moves to DOT and all funds over the $300 also go to DOT.

4. Control Component: This proposal includes two controls designed to prevent dramatic changes to gas prices from affecting the revenues dedicated to infrastructure.

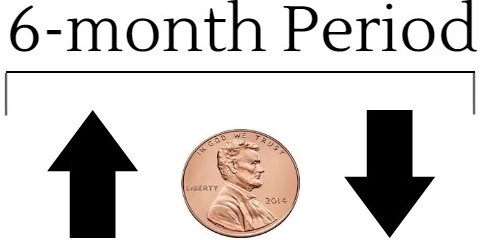

A. Penny Control

- The wholesale excise tax would not fluctuate more than one penny in a 6-month period.

B. Lifetime Control

- The combined gas tax (comprised of the per gallon AND excise) cannot exceed 26.75 cents/gallon.

5. Revenue Generated:

A. Estimated New Revenue: Under this proposal revenues generated would be $428 million annually.

- Approximately $100 million from the auto sales tax cap increase, and shift of remaining General Funds to DOT.

- The remaining $328 million from the gas tax increase.

B. Gas Tax Revenue Sources

- Out-of-State motorists currently comprise 1/3 of the revenues from the gas tax. Under this proposal that would equal $109 million.

- The Average driver (driving 11,000 miles/year in a car receiving 22 miles per gallon) would pay an additional $50 annually.

- The remainder is paid by “high usage vehicles” to include citizen commuters and transportation related industry.

6. Income Tax Reduction: Under this proposal an income tax reduction would be phased in over a two-year span beginning with fiscal year 15-16. The relief is realized by increasing the amount of exempt income in each existing tax bracket by $140 in the first phase, and another $140 the second, for a combined total of $280.

A. Cost to the General Fund

- 2015-2016: $1,337,967

- 2016-2017: $25,510,778

- 2017-2018: $21,910,558

B. Average Savings

- The average South Carolina taxpayer would save $48 annually.